frankpeters/iStock via Getty Images

Do you want to read an absolutely (even insultingly) obvious statement?

Since I can’t hear any dissent to that question – and therefore take the silence as resounding consent – here it is…

As I write this, the markets are down for the year.

Told you it was absolutely (even insultingly) obvious. But there it is, nonetheless.

For the record, the markets are down for the day as well while I type these words out. And, considering how things have been going, there’s an unfortunate chance they’re down as you’re reading this, too.

The investment world just isn’t happy at the moment. Obviously.

I could go on about all the reasons why it’s not happy: Inflation, the Fed, continuing shortages, and other company-constricting issues.

But what would be the point?

You already know it all. It’s been in your face all year: more than 130 days of dealing with this… stuff… both on an investment level and a personal one.

Back on April 30, MSN published a piece titled, “The S&P 500 Is Down [13.8%] in 2022, the Worst Year-to-Date Performance Since World War II.”

And that was when:

- The S&P 500 was down to 4,131.93.

- The Dow was down to 32,977.21.

- The Nasdaq was down to 12,334.64.

As opposed to December 31, 2021, when:

- The S&P 500 ended at 4,778.73.

- The Dow ended at 36,398.08.

- The Nasdaq ended at 15,644.97.

Oh how the mighty had fallen.

Are We There Yet? (We’re Getting Carsick!)

As of the close on May 11, those figures were 3,935.18, 31,834.11, and 11,364.24, respectively. So there was clearly further to fall.

Considering how many times that’s been true so far this year, it’s left many an investor on edge. If anything, the upticks we’ve seen here and there may have only exacerbated fears.

To many, it seems like nothing is predictable right now. And the lack of predictability can be downright scary.

I’m going to take a moment here to emphasize one word in that paragraph above: many. If you’re not sleeping well at night these days because of your investments, you’re not alone.

Not even close.

For proof of that, consider how the very well-known and very much-watched Jim Cramer felt the need to reassure his audience the other day. According to this MoneyWise writeup, he believes:

“… the recent plunge in stocks reflects a lack of investor confidence in the Federal Reserve. He says these investors believe that the Fed has lost control or is helpless to fix things given the state of the global supply chain.

All true.

“But Cramer remains bullish – particularly on Fed Chairman Jerome Powell. ‘I think the consumer is strong. Jobs are plentiful,’ he says. ‘Leaving the market is a mistake because Powell happens to be an incredibly thoughtful, good public servant who’s doing amazing.’”

Debatable. Very, very debatable. Except for the part about staying in the market. I completely agree with him there.

It’s just a matter of knowing how and where.

REITs Are Showing Amazing Resilience

With all due respect to Cramer, he doesn’t always have the greatest track record. So I stopped reading the aforementioned article after the very next paragraph, which read:

“For bullish investors who share that sentiment, here are a few [of] Cramer’s top recommendations.”

I’m just not going to spend time there when I have a great team of analysts who are constantly compiling excellent research on dividend-paying stocks, international investments and, of course, real estate investment trusts ((REITs)).

iREIT on Alpha and its sister service, Dividend Kings, are confident – not only in our current recommendations but also the prospects in front of us.

As I was telling a friend the other day, even though the markets are down, REIT rent checks are not. Property value isn’t down either. And, as a result, REIT earnings are stronger than ever.

Some of you may have read the Benzinga article the other day, “Warren Buffet Doesn’t Buy Real Estate – Here’s Why Most Investors Shouldn’t Either.” But that title is misleading, as the writeup itself admits:

“Buffett isn’t against investing in real estate. In fact, he has invested in several… REITs… over the years. However, he knows it makes little sense for him to get into the business of being a landlord.”

Fair enough. Even agreed. It’s very difficult to be a successful real estate investor on your own – something I know a thing or two about.

There’s finding or building the right properties in the right places… then determining the right tenants under the right lease agreements… then retaining the right tenants who can afford to pay rent.

And that says nothing about property taxes, insurance, and

the like.

But REITs do all that heavy lifting. And, as I said above, they’re still collecting rent and shelling out dividends-a-plenty.

3 REITs We’re Buying Hand Over Fist

Please understand me: I fully understand concerns about steep inflation and its effect on our investments. With that said, money flows in REIT-dom continue to be strong, with interest rates merely normalizing.

All things considered, they’re still low historically.

It appears that investors have increasingly priced in a recession to stock valuations – though asset pricing will continue to be volatile in the near term. Plus, many economists don’t see a recession until 2024.

Overall fundamentals remain strong regardless. And spending shows no signs of meaningful decline, with small-to-medium sized businesses looking to grow.

This is why we remain bullish about dividend-paying stocks. We believe investors should be ready to deploy capital toward strong, stable cash-flowing companies.

There are quite a few high-quality REITs that are being priced at pandemic levels right now. So iREIT on Alpha is taking advantage of the current volatility by building core positions with names that can grow healthy dividend payouts.

Naturally, as we scan the equity REIT universe, we’re most interested in stocks that offer solid growth prospects, healthy balance sheets, and cheap pricing. By utilizing our iREIT Tracker tool, we find three very compelling opportunities:

- Innovative Industrial Properties, Inc. (IIPR)

- Digital Realty Trust, Inc. (DLR)

- Realty Income Corporation (O).

Let’s take a look at each one of them in turn…

Capitalizing On The “Volatile” Innovative Industrial

(IIPR website)

Innovative Industrial Properties is a cannabis-focused REIT that was founded in December 2016, Since then, it’s become the first company on the New York Stock Exchange to provide real estate capital to the regulated cannabis industry.

IIPR owns 109 properties with over 8.1 million rentable square feet in 19 states. Annual revenue at the end of Q1-22 was around $258 million, and commitments and investments totaled $2.2 billion.

IIPR’s business model centers on U.S. cannabis operators that have an outsized need for capital. U.S. regulated cannabis sales will grow an estimated $46 billion by 2026, almost double 2021’s estimated $24 billion.

As of February 4, 2022, 38 states and Washington, D.C. had legalized cannabis for medical-use. And 18 states and Washington, D.C. allow adult-use as well.

However, cannabis operators must still obtain proper state licensing, which is becoming more and more competitive. That gives IIPR a moat-worthy business model worth investigating, which it expertly exploits.

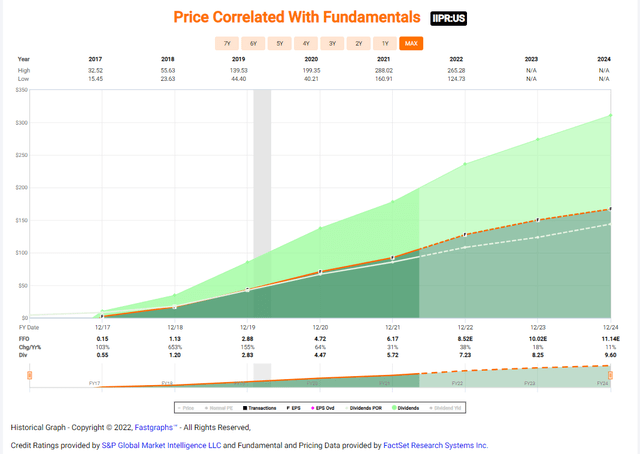

The company continues to deliver rock-solid growth fueled by a successful history of capital raising. As viewed below, IIPR has delivered best-in-class adjusted funds from operations (AFFO) per-share growth and very predictable dividend growth too:

(Fast Graphs)

And even though marijuana federalization is an eventual possibility, legislation isn’t the death knell some say it will be. We suspect that if and/or when that happens, IIPR will still be able to grow earnings at noteworthy rates.

In the meantime – especially since our sources say that likelihood remains a few years out – we believe it makes the most sense to make hay while the sun is shining.

IIPR also has very modest leverage at just around 15% debt to assets. This means it can always increase leverage if needed to enhance AFFO per share.

Innovative Industrial Properties Continued

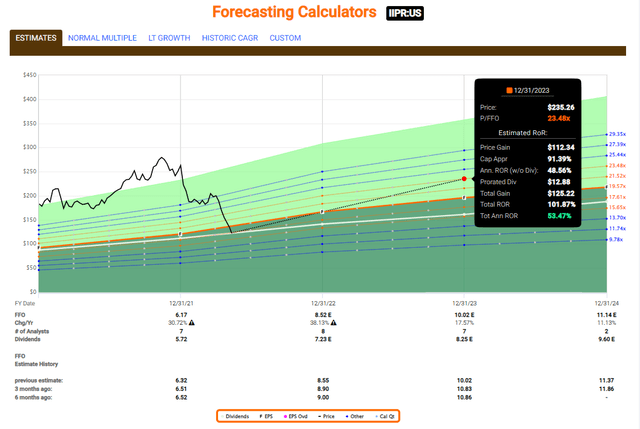

What we find most compelling is how it’s trading at a lower multiple today than it did during March 2020. Essentially, Mr. Market is pricing IIPR shares as if cannabis is a cruise line heading into another pandemic.

Never mind that this company is in the best business shape ever. It has collected 100% of rents and cannabis sales are estimated to grow to $46 billion by 2026, almost double 2021 estimated regulated sales of $24 billion.

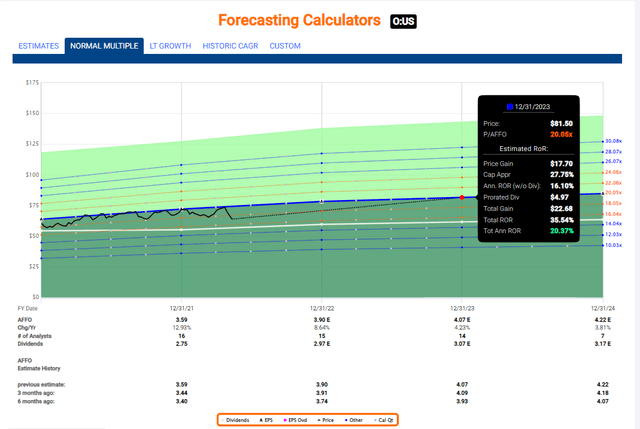

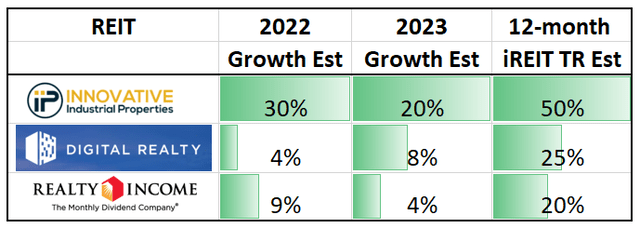

Our conservative model has IIPR returning 50%+ over the next 12 months. That’s based on analyst growth estimates of 38% in 2022 and 17% in 2023.

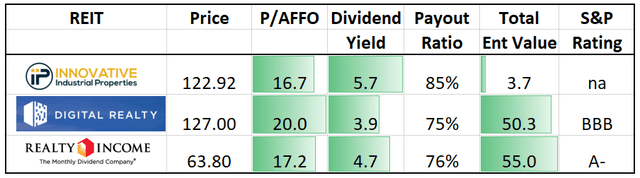

Shares currently trade at $122.92, with a p/AFFO of 17.5x compared with March 2020’s 18x. Their dividend yield is 5.7% – which I find truly astonishing given the company’s healthy 85% payout ratio and strong rent collection.

But, hey, we’ll take it!

One common thread with all three of this article’s REITs is they’re the No. 1 players in their respective sectors. So, during this kind of uncertainty, we’re more than happy to take advantage of their volatile prices.

(Fast Graphs)

Capitalizing On The “Volatile” Digital Realty

(DLR website)

Digital Realty is a leading data-center REIT that went public in 2044 with 21 properties. Today, it owns 280 in 26 countries on six continents.

I’ve owned it since 2013, and shares have returned an average 20% annually for me.

DLR boasts the largest global platform of multi-tenant data-center capacity: 170,000+ cross-connects in critical locations for 4,300+ customers.

We like data center REITs in general because of their strong demand drivers. They’re well-protected against rising energy costs given the pass-through nature of substantially all their

customer contracts.

Recently, IDC updated its global data sphere forecast for 2025. The industry research firm predicts DLR’s annual data creation rate will exceed 180 zettabytes – roughly triple its 2021 rate.

IDC expects companies of all sizes will need to prioritize data sharing and security to improve business resiliency and create differentiated experiences for their customers.

This thinking is validated by DLR’s healthy operating results. In Q1-22, it had $167 million in total bookings signed with an $11 million contribution from interconnection. This is its second consecutive quarterly record and the seventh time in the last eight quarters it’s delivered bookings over $100 million.

Also, DLR’s current backlog of leases signed but not yet commenced grew 15% to a record $436 million. And signings outpaced commencements.

DLR did announce a tenant bankruptcy in Q1. However, it’s maintaining its 2022 core FFO per-share range of $6.80-$6.90.

Its financing strategy, meanwhile, reflects the strength of the global platform that provides access to both public and private capital.

The company’s weighted average debt maturity is over six years, and its weighted average coupon is 2.2%. Over 90% of that debt is fixed rate, and 99% is unsecured for excellent capital recycling flexibility.

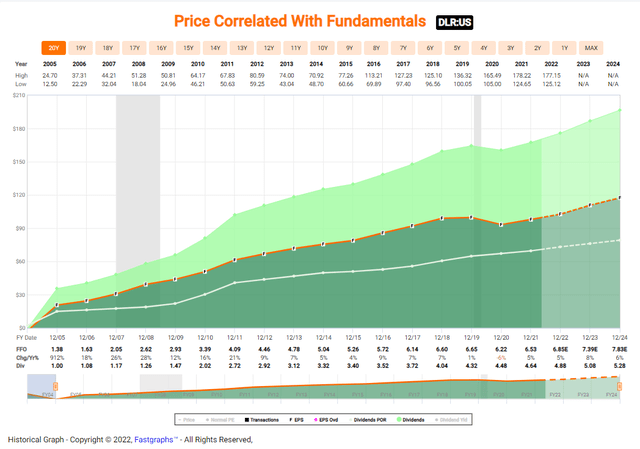

As viewed below, DLR has maintained very predictable earnings and dividend growth:

(Fast Graphs)

Digital Realty Continued

Earlier this week, we informed iREIT on Alpha members that DigitalBridge (DBRG) and IFM are acquiring Switch (SWCH). The all-cash $34.25-per-share should close in Q3-Q4.

At about an $11 billion enterprise value, the deal represents 27.6x the company’s estimated 2023 AFFO. By comparison, consider these past acquisitions:

- CoreSite for 30x its estimated 2022 AFFO

- CyrusOne for 22x 2022E

- QTS for 29.5x 2021E.

As such, “few publicly traded data center platforms remain.” This should reflect positively on both its valuations at 19.9x 2022E p/AFFO and Equinox’s (EQIX) 22.6x.

In fact, the Switch information validates our evaluation that DLR is one of the cheapest data center trades today.

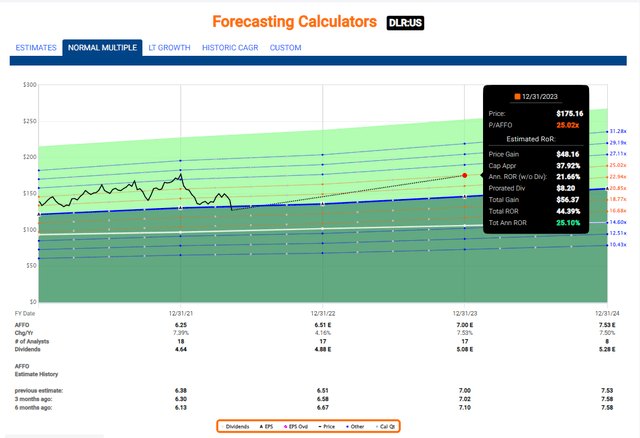

Shares are currently trading at 20x p/AFFO versus its 19x in December 2019 and five-year multiple of 19.5x. While some would argue that’s “fair” value right now, we give it premium value because of its powerful cost of capital and scale advantages.

Analysts forecast just 4% growth this year. But that should increase to 8% in both 2023 and 2024. And DLR’s current dividend yield is 3.8%.

As viewed below, our 12-month model has it returning 25% driven by a 2023 year-end multiple of 25x. Moreover, we view this as conservative.

Given everything listed above, this data giant should generate superior return on equity (ROE).

(Fast Graphs)

Capitalizing On The “Volatile” Realty Income

(O website)

Realty Income is a dominant net-lease REIT that was established in 1969 and listed in 1994. It owns over 11,000 properties in 50 states and Europe.

Better yet, it’s a dividend aristocrat having increased dividends for 28 consecutive years.

O has over 1,000 customers in 60 different industries. Around 94% of total rent is resilient to economic downturns and/or isolated from e-commerce pressures.

The company has 4.7% exposure to gyms and 3.4% to theaters. Yet it managed to grow earnings (i.e., AFFO per share) during the worst of Covid-19 – one of just three net-lease REITs that did.

It’s generated 5.1% median growth since 1996, stronger than REITs in general at 3.9%. And it’s seen positive earnings growth in 25 of 26 years, with modest annual downside volatility of 2.8%.

O’s proven track record of maintaining 5%+ earnings compound annual growth rate (“CAGR”‘) has accelerated. Portfolio real estate value has now crossed $10 billion, with 6.4% AFFO/share CAGR since 2012.

Recently, O announced the purchase of Encore Boston Harbor (Encore) Resort and Casino for $1.7 billion. That makes for a 5.9% cash cap rate with a 30-year triple-net lease and favorable annual escalators.

This entry into the gaming industry demonstrates that Realty Income’s growth opportunities remain notably unconstrained.

As-is, its balance sheet is rated A3 by Moody’s and A- by S&P – making it one of just seven REITs with A-rated balance sheets.

The company entered 2022 strong, with a net debt to annualized pro forma adjusted earnings before interest, taxes, depreciation, amortization, and restructuring or rent costs (EBITDAR) of 5.3x. And it has ample liquidity to capitalize on acquisition opportunities, with around $1.5 billion on the revolver and $259 million in cash.

Recently, O announced its 622nd consecutive monthly dividend at $0.247, representing an annualized $2.964.

(Fast Graphs)

Realty Income Continued

With the successful integration of VEREIT’s assets, analysts expect AFFO per-share growth of 9% in 2022. This will make it one of the highest growth REITs this year.

And, given its well-positioned balance sh

eet, we wouldn’t be surprised to see more mergers and acquisitions (M&A) deals. Maybe Spirit Realty (SRC) or Gaming & Leisure (GLPI)?

And O could also seek out more big sale-leasebacks in the gaming sector, where cap rates remain attractive. Or try on the entertainment category for size with such names as Six Flags (SIX).

Of course, while O is arguably the healthiest it’s ever been, Mr. Market doesn’t see it. Shares are trading below its 2021 multiple average of around 20x to now sit at 17.2x.

In fact, over the last eight years, O’s average p/AFFO has been 19.7x, which validates the overall cheap valuation of this dividend dynamo.

So, no matter what Mr. Market says, we know the outcome of this drama already. O is perfectly positioned to combat rising rates – even as cap rates compress – with several levers it can pull to grow earnings.

Don’t underestimate Realty Income’s sheer size and power – or the fact that it has such a large pond to fish in with its new European focus on top of its U.S. options.

O’s dividend yield is currently 4.7% and well-covered. So we forecast shares could return about 20% over the next 12 months.

Once more, scale has its advantages, and O has all of the ingredients for something very special. Realty Income is my largest portfolio position. And thanks to dividend reinvesting, it just continues to compound.

(Fast Graphs)

Buy These Safe Havens

I’ve provided you with three “safe-haven” REITs that boast highly predictable earnings and dividend growth. And their leadership is top-notch too.

As part owners of these businesses, we’re paying the C-suites’ salaries. So we definitely expect them to generate attractive shareholder value.

After meeting with management, touring their properties, and analyzing their data up and down… we’ve concluded that their potential for long-term value creation is above-average to excellent.

(iREIT on Alpha) (iREIT on Alpha)

Down here in my neck of the woods, I drive by a shopping center – that I once owned – almost daily. And it’s always packed, suggesting that rents are getting paid and the asset itself is retaining value.

Yet REITs are on sale, trading at a 50% discount in some cases, as with IIPR.

In short, REITs are extremely attractive right now. And it doesn’t take a $50 million net worth to get a piece of the action.

Warren Buffett once spoke of the price of hamburgers at McDonald’s (MCD) as a stock market analogy. If the price tag is reduced, he noted, he doesn’t get worried; he just buys more and feels good that he’s paying less.

Of course, as he also acknowledged, overcoming fear is easier said than done.

“There is no comparison between fear and greed. Fear is instant, pervasive, and intense. Greed is slower. Fear hits.”

Nonetheless, volatility means opportunity! That’s why I continue to add shares in these three REITs and others, as recommended to members at iREIT on Alpha.